Zeitgeist: Why (or Why Not) Cryptos, Part 1

Zeitgeist: Why (or Why Not) Cryptos, Part 1

A Short Note About The Dollar (and Other Things) to Start Off With

The “Zeitgeist” series aims to take apart a phenomenon that has captured public interest. Thus, the analysis would cover a phenomenon still in progress. This time, the “Zeitgeist” has cryptocurrencies in its sights. While not quite as verbose as the six-part series that examined the electric vehicle industry, this would be still done over two parts. To drive context, we need to start with the “almighty” U.S. dollar. The quotation marks are purely intentional.

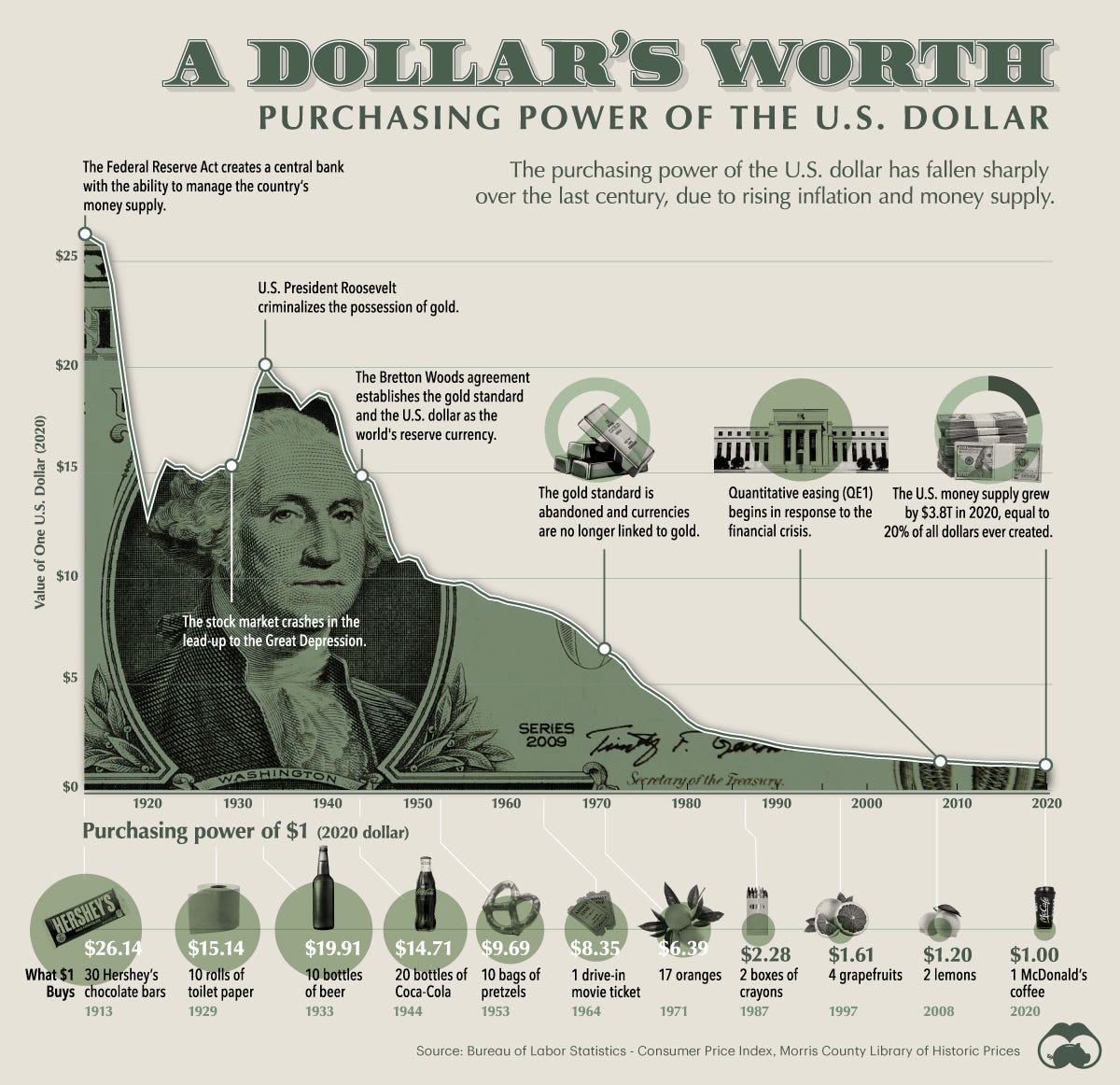

In 1913, the U.S. Federal Reserve Act granted Federal Reserve banks the ability to “manage” money supply in order to ensure economic stability. When more dollars were entered into circulation, the average prices of goods and services increased while the purchasing power of the dollar fell. By 1929, the value of the Consumer Price Index (CPI) was 73% higher than in 1913. Corrections made by contracting the money supply by 31% which actually caused a deflation between 1929-33, thus increasing the purchasing power of the U.S. dollar. Deficits caused by World War II, the Korean and Vietnam Wars, the Cold War, etc., etc. led to more and more dollars entering circulation. By 1971, the U.S. government ended the gold backing of its currency since the number of dollars in circulation had by then long outstripped the value of U.S. gold reserves.

Interestingly, one feature of the 1944 Bretton Woods conference was the establishment of an “adjustably pegged foreign exchange market rate system” with the exchange rates pegged to gold. The U.S. dollar was pegged at $35/oz and become the favoured reserve currency for participating nations in the conference ratifying the agreement in 1946 (except for the U.S.S.R, which protested the inclusion of the US$ alongside gold). Despite the U.S. government abandoning the “gold standard”, US$ continued being favoured as a “reserve” currency by institutions and governments around the world - almost all of the latter had abandoned the “gold standard” as well.

The U.S. dollar has had a wild ride through the ages: $1 in 1913 had the same purchasing power as $26 in 2020.

Let’s switch tracks to take a look at another indicator of U.S. prosperity: the S&P 500 (SPX). Introduced in 1957 track the value of 500 large NYSE-listed companies, the value of the index rose to nearly 700 in its first decade, reflecting the post-WWII economic boom in the U.S. Since its inception, it has proven to be a fairly robust indicator of U.S. economic health: the index declined from 1969-1981 while the U.S. economy endured stagnant growth and high inflation, fell almost 58% during the 2008 financial crisis and recovered nearly all its losses brought about by the 2008 crisis by March 2013, which was its third year of a 10-year bull run when the SPX climbed nearly 400%. Of course, the coronavirus pandemic - temporarily - brought own the SPX by 51% in 2020, leading to all-time high of nearly 4,019.87 on April 1, 2021.

A common trope indicating the strength of the U.S. economy is as follows:

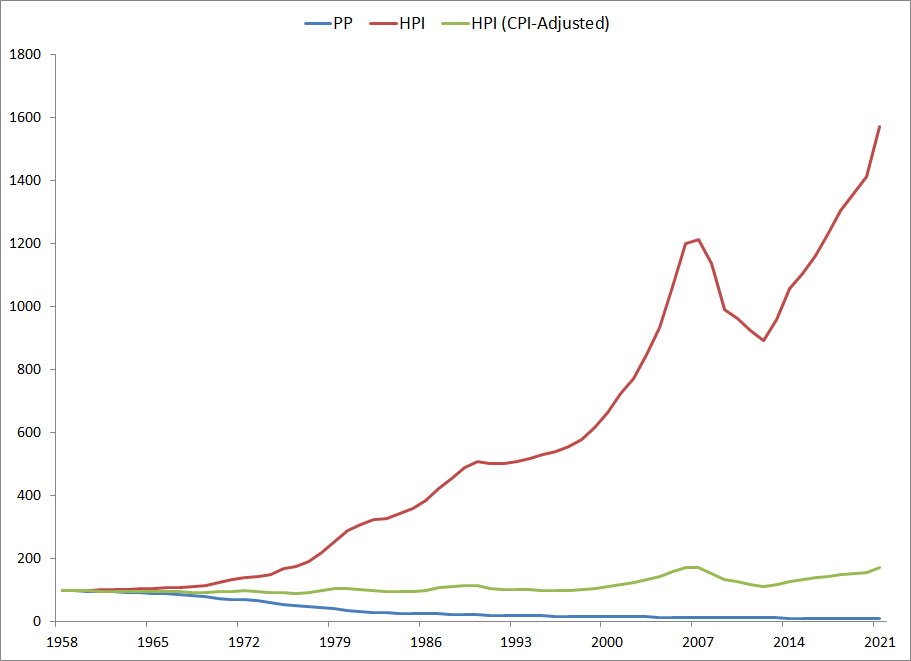

If you, dear reader, had invested $100 in the S&P 500 index in 1958, your investment would be worth $57,673.66 in 2021.

This is, however, a nominal value as it doesn’t incorporate inflationary effects on the U.S. dollar. Refactoring S&P 500 monthly performance with US$ purchasing power from Federal Reserve Economic Data (FRED), we arrive at this rather ominous graph:

This graph shows the comparative performance of 100 “real” dollars (100 1958 US$ subsequently adjusted for purchasing power) and the “real” S&P level (100 1958 US$ invested into the SPX and subsequently adjusted for purchasing power) versus the reported (or “nominal”) SPX values. As it turns out:

If you, dear reader, had invested $100 in the S&P 500 index in 1958, your investment would be worth $6,141.32 in 2021 in terms of 1958 dollars.

The US$ isn’t the only confounding factor in wealth-building in the U.S. The U.S. National Home Price Index, established by Nobel Laureate Robert Shiller, shows a different woe with regard to home equity:

While in nominal terms, the prices of homes have galloped well ahead of what it would have cost in 1958, home prices - even when adjusted for inflation - shows that a home would cost 71% more in 2021 than in 1958 even in terms of 1958 dollars. Suddenly, all those hit pieces on Millennials by *sigh* journalists begin to sound like low blows, don’t they*?

*Journalists really need an education in economics. But, meh, what do I know? I’m sure it’s hard writing words filled with feelings.

A key feature of economic powerhouses is the “knowledge economy”. Invariably, that means a college education is the stepping stone to producing skilled workers. The U.S., in addition to its mineral resources, also boasts an extensive network of educational institutions that have burnished the nation’s edge in knowledge-intensive fields. However, even in this category, the runaway effects of second-order inflation (i.e. inflation not linked to the currency’s purchasing power) are quite evident:

It can be seen that, unlike home prices which saw a paltry 71% inflation-adjusted increase in cost for home equity buyers from the late fifties, a 4-year college education has seen an over-400% inflation-adjusted increase from approximately the same time. This, of course, will have a deleterious effect on wealth-building by young workers entering the economy.

How About The Rest of the World?

It can be safely assumed that home prices and cost of education has been on the rise all over the world1. However, a quick analysis is possible - outside of baseline costs on education and home equity - on other goods and services.

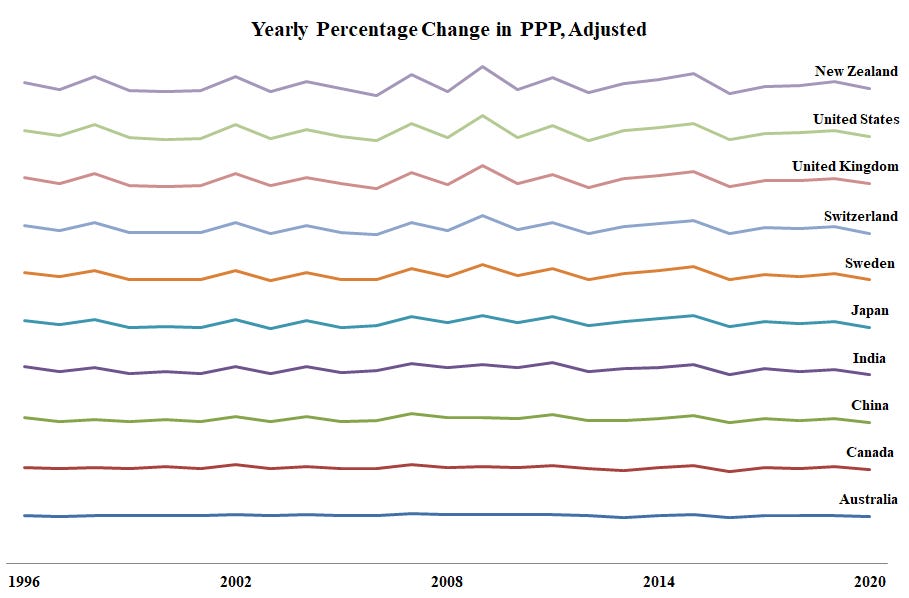

Purchasing power can be tweaked into a pretty handy measure to estimate the relative economic similarity between nations. Purchasing Power Parity (PPP) postulates that two currencies are in equilibrium when a basket of goods is priced the same in both countries after taking into account the exchange rates. As per the Organisation for Economic Co-operation and Development (OECD), here is what the year-on-year change in PPP centered around the inflation-adjusted 1996 US$ dollar looks like for a selection of the leading/most-mentioned countries in the world from 1996 to 2020:

Barring Australia and Canada, there is a perceptible “East vs West” difference in terms of cost stability (the fact that both Australia and Canada have lately been “resource economies” likely has an influence on their stability relative to other Western countries; the rest are economic powerhouses with the skills of its citizenry being a leading factor). But, in general, the East seems to be a little more stable in terms of PP change than the West.

But What Does it Mean, Sensei?

An interesting challenge - entirely separate from the question of cryptocurrencies - emerges for the U.S.’ knowledge economy: first- and second-generation immigrants have been a major source for the lifeblood in this sector for quite some time now. A substantial proportion of said lifeblood come from India and China, both of which are powering up to for the “World’s #1” position in this century.

Given the egregious cost of wealth-building - both in home equity as well as education - it is increasingly economically reckless for the first generation to trade in its “hometown advantage” for foreign shores (the first generation’s successors will, in particular, face higher barriers to wealth-building; their parents, being Fresh Off the Boats (FOBs), had at least some of the costs pared down due to a portion of their education earned in their home countries).

Outside of this, there are two key points in terms of wealth-building in the U.S. (in particular and the West in general):

Acquiring home equity is the only viable means of recouping/surpassing lost purchasing power. This is evidenced by the increasing number of hedge funds focused solely on real estate acquisition. Note: “Acquiring” here means purchasing wholesale. Adjustable interest rates on home loans definitely pare down recouped value (often down to loss-in-purchasing-power levels or worse), thus making the entire process more expensive than when entered into.

Being invested in the stock market is the most viable means of maintaining wealth along the purchasing power trajectory. The importance of IRAs over traditional savings ensconced in a bank account cannot be emphasized enough.

The high cost of both (1) and (2), however, skew success away from the general population in the U.S. and towards a increasingly smaller set of people in the U.S. and the West. And this is the first hint as to why cryptocurrencies are so dominant in the public eye.

But more about cryptocurrencies next week.

This brings us to the end of Part 1 of the “Zeitgeist” on cryptocurrencies. The next (and concluding) entry colours in the background with some insight on the possible major movers of the crypto space and some final thoughts. Stay tuned and hit “Subscribe” here if you haven’t already!

Take my word for it, dear reader. Compiling and posting all of that here would be a major “mendokusai” (めんどくさい). It’s a FREE newsletter!